As the crisis in the Middle East unwinds with no ceasefire in sight, it is worth analyzing and understanding the impact of these events on the emerging markets, which compromise 52% of the world’s population. Last year, MSCI EM total return came in at 34.36%, decisively outperforming the S&P 500 for the first time since 2020. The S&P 500 delivered a total return of 17.9% in 2025.

However, since most nations in EMs are net energy importers (see Figure 1) and are very prone to energy crises, investors are rotating away from EMs amid growth and stagflation fears. Therefore, as energy supplies and infrastructure as well as production and extraction facilities are disrupted (which will take from 3 months to 2-3 years to repair), combined with increased risk aversion for investment in the Middle East region (meaning that future potential productivity capacity is reduced), the shortage of oil, gas, fertilizers, and other key natural resources required for economic activity is likely to persist with resulting elevated prices. It means that now EM countries might see their current account deficits widening, currencies depreciating, growth compressing, credit conditions tightening, and inflation spiking. I will explore these impacts in more detail to better understand the future of these nations, but for now let’s consider the macroeconomic landscape at a glance (see Figure 1).

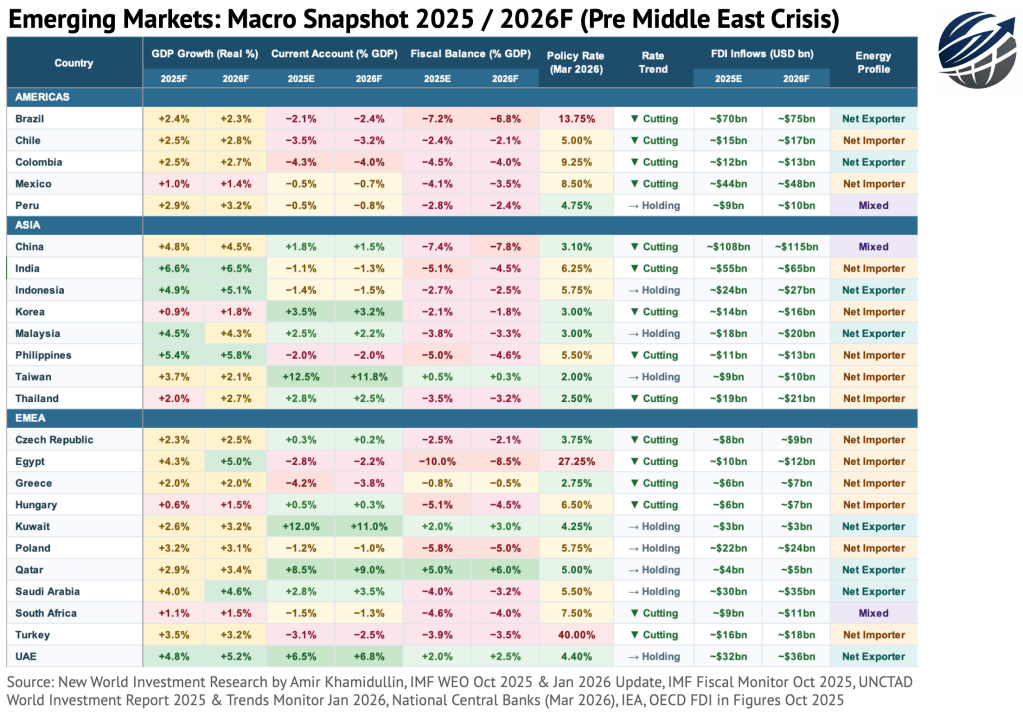

For a PDF of the chart, please see below.

Rate policy: Zero hikers across the entire 24-country universe. This is historically unusual. The GCC “holders” (Saudi, UAE, Kuwait, Qatar) aren’t hawkish by conviction; they’re mechanically pegged to the Fed and have no independent rate-setting role.

Fiscal: The picture is bleak outside the Gulf. 21 of 24 countries are running deficits, with Egypt at −10% GDP the most dangerous given it’s paired with a current account deficit and no commodity revenue buffer. Brazil (−7.2%) and China (−7.4%) are the large-economy problem cases: both face debt trajectories that compound without consolidation.

Energy exposure: 12 of 24 countries are net energy importers, meaning any sustained oil spike hits their CA balance, fiscal subsidies, and inflation simultaneously. India, Korea, Turkey, and the Philippines are the four most systemically important importers given their size and import dependency.

Current account: Taiwan (+12.5%) and Kuwait (+12%) are in a class of their own – both structural surpluses driven by manufacturing dominance and hydrocarbon exports, respectively. Colombia (−4.3%) and Chile (−3.5%) are the most vulnerable, as they are commodity exporters with structural CA deficits, which is a particularly fragile combination when global growth slows.

Growth divergence: Asia is simply in a different category. Strip Korea out and every Asian EM is growing above 4%. The Americas bloc is sluggish across the board (1–2.9%), and EMEA is bifurcated between the Gulf outperformers and the European EMs stagnating below 2%.

The bottom line is that given the ongoing dynamics in Iran and the Middle East, the macro case with which EMs entered 2026 will change significantly, and unfortunately not in the favor of these economies.

—

Follow for more research & insights at amirkh.com

By Amir Kh.

Leave a comment