-

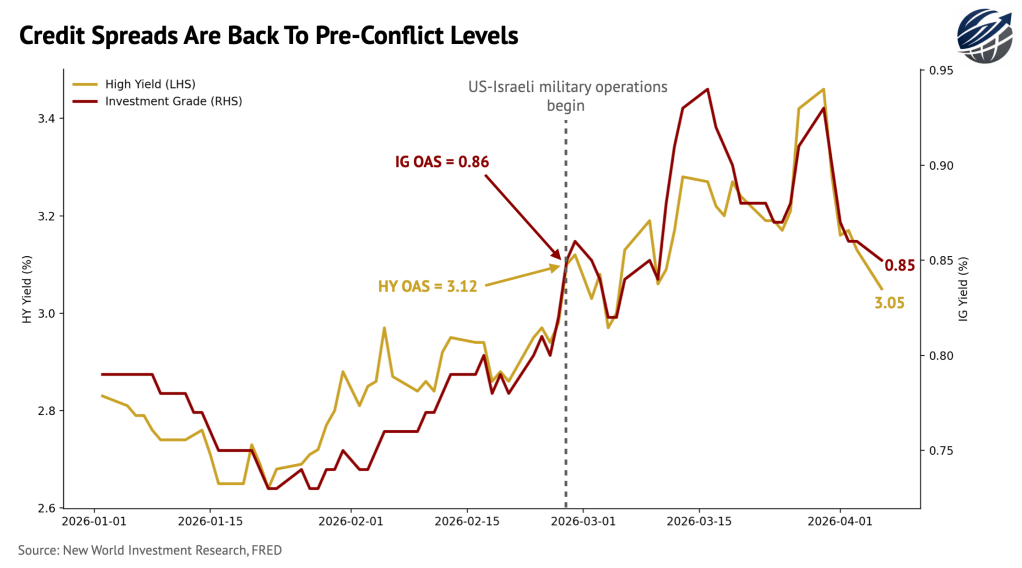

Credit Spreads Are Back To Pre-Iran Conflict Levels

Credit spreads are back to pre-Iran conflict levels. HY OAS is back around 3.05% versus ~3.12%…

-

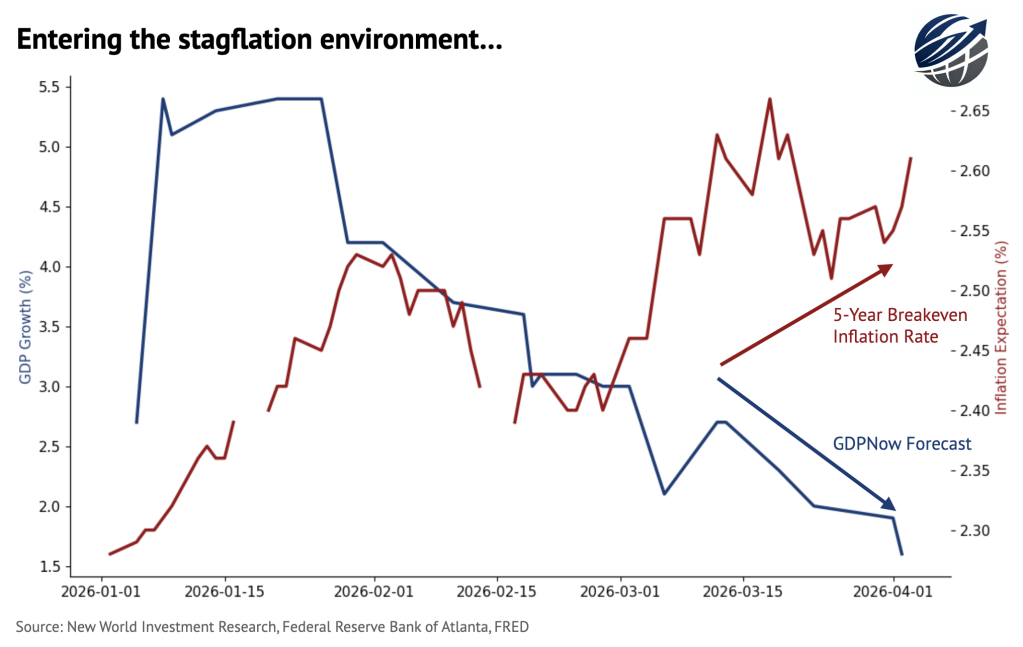

Entering the stagflation environment…?

The current data from the Federal Reserve Bank of Atlanta points to lower GDP growth forecasts,…

-

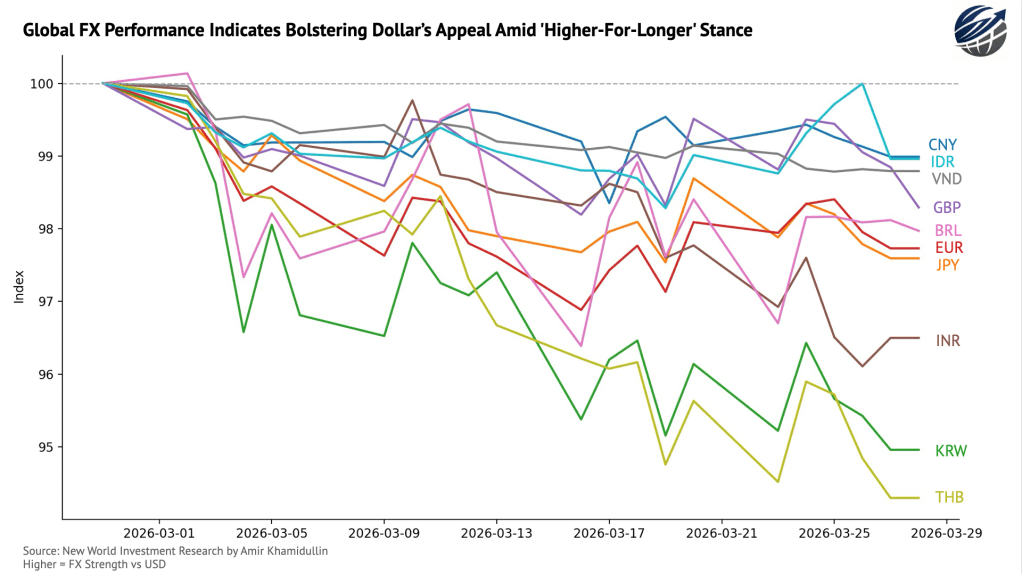

A Strengthening Dollar And A Weakening… Well, Everything Else!

As markets are pricing higher inflation, disruptions in supply chains, and widening energy shortages, central banks…

-

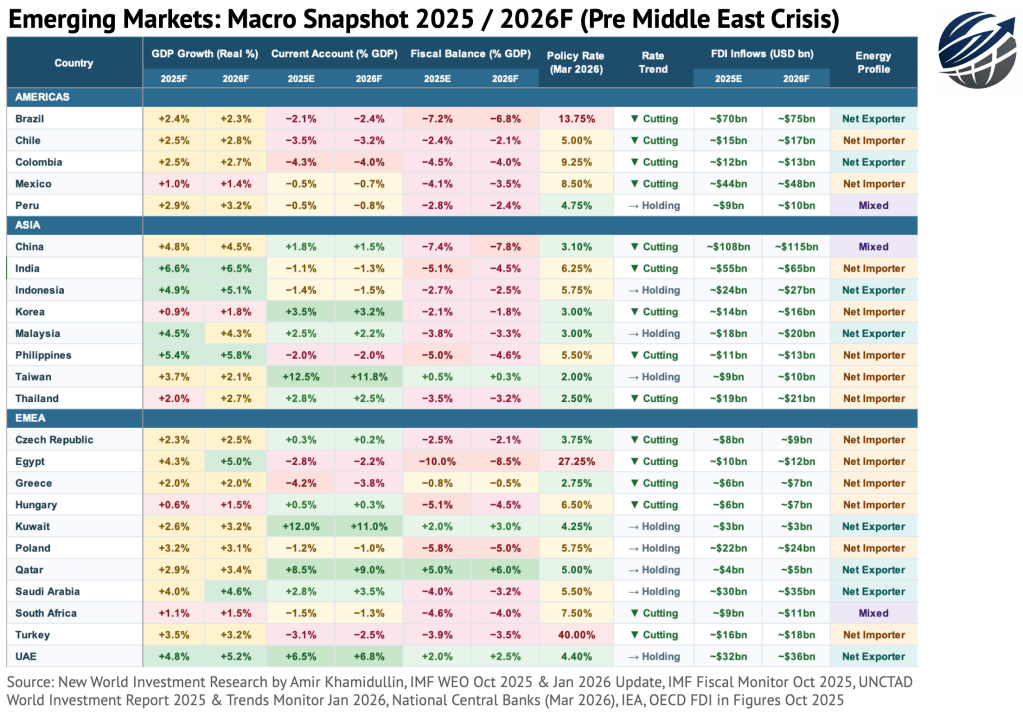

EMs: Macro Snapshot 2025/2026F

As the crisis in the Middle East unwinds with no ceasefire in sight, it is worth…

-

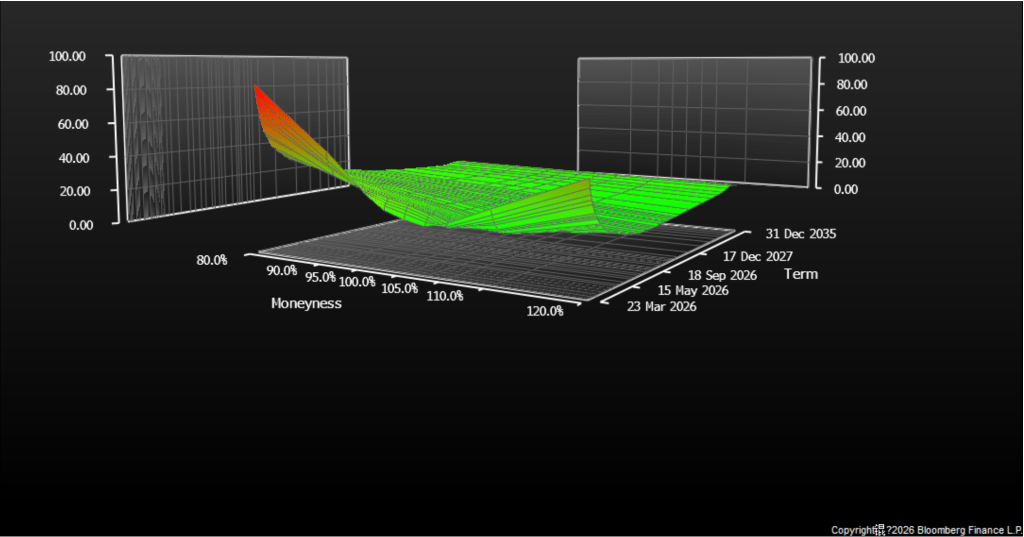

Options Are Pointing To Near-Term Fear Rather Than Structural Long-Term Repricing

The S&P 500 implied volatility surface gives some interesting observations. Near-term put skew spiking to 80-100…

-

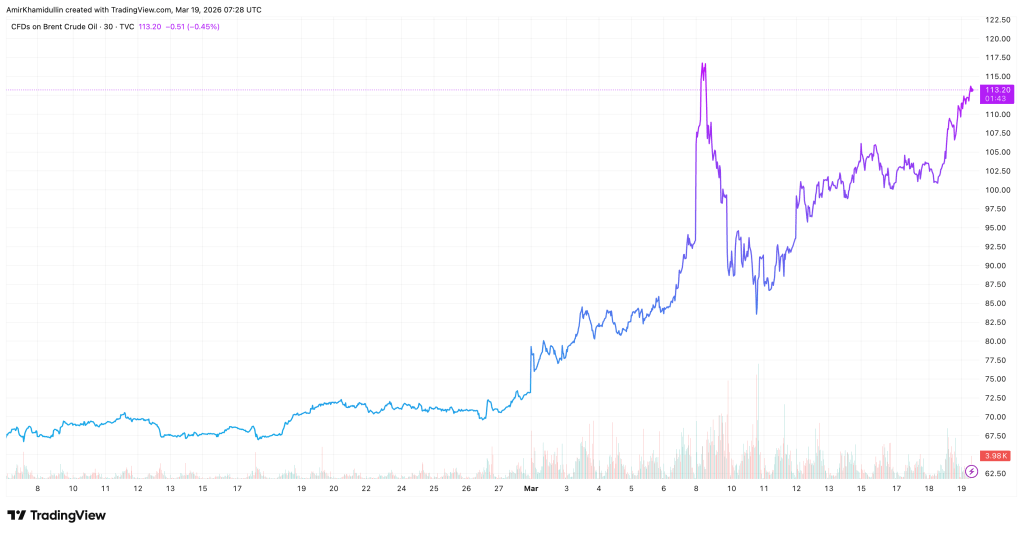

This Isn’t Just An Oil Shock…

As the conflict in Iran unwinds further with deeper escalations happening on a daily basis, it…

-

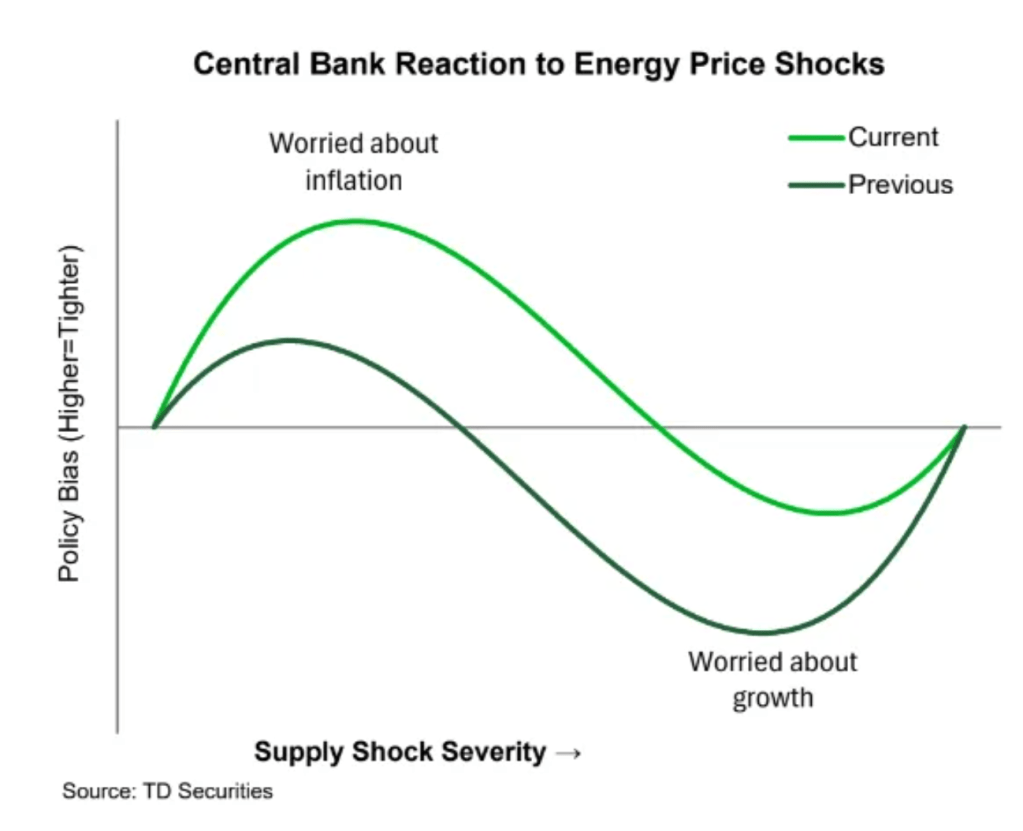

Are Central Banks Overreactive To Supply Shocks?

As central banks across the world are deciding on their policy trajectories given energy supply shocks…

-

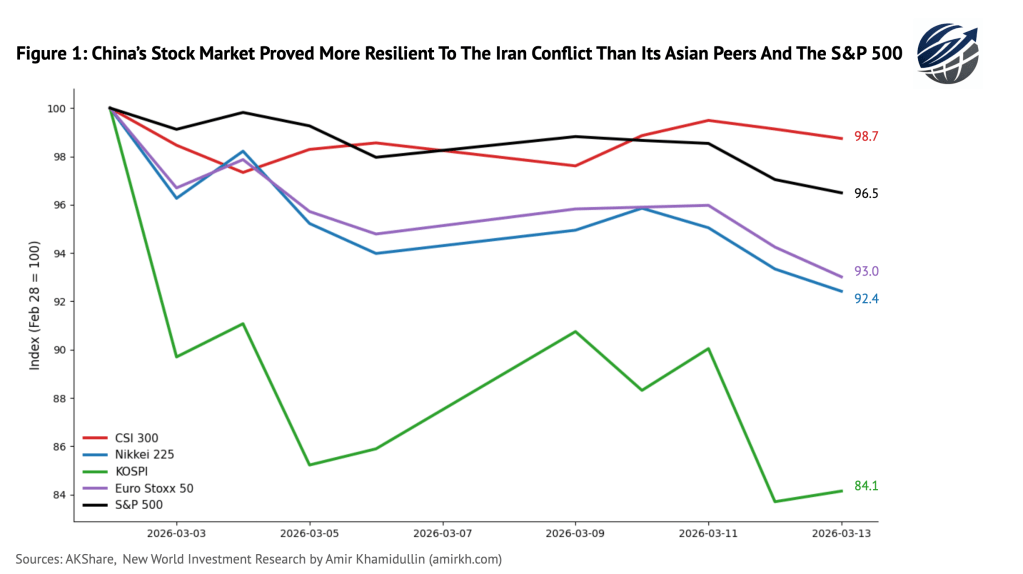

CSI Resilience Amid Oil Crisis

China’s equity market has shown notable resilience during the recent escalation around Iran. While several major…

-

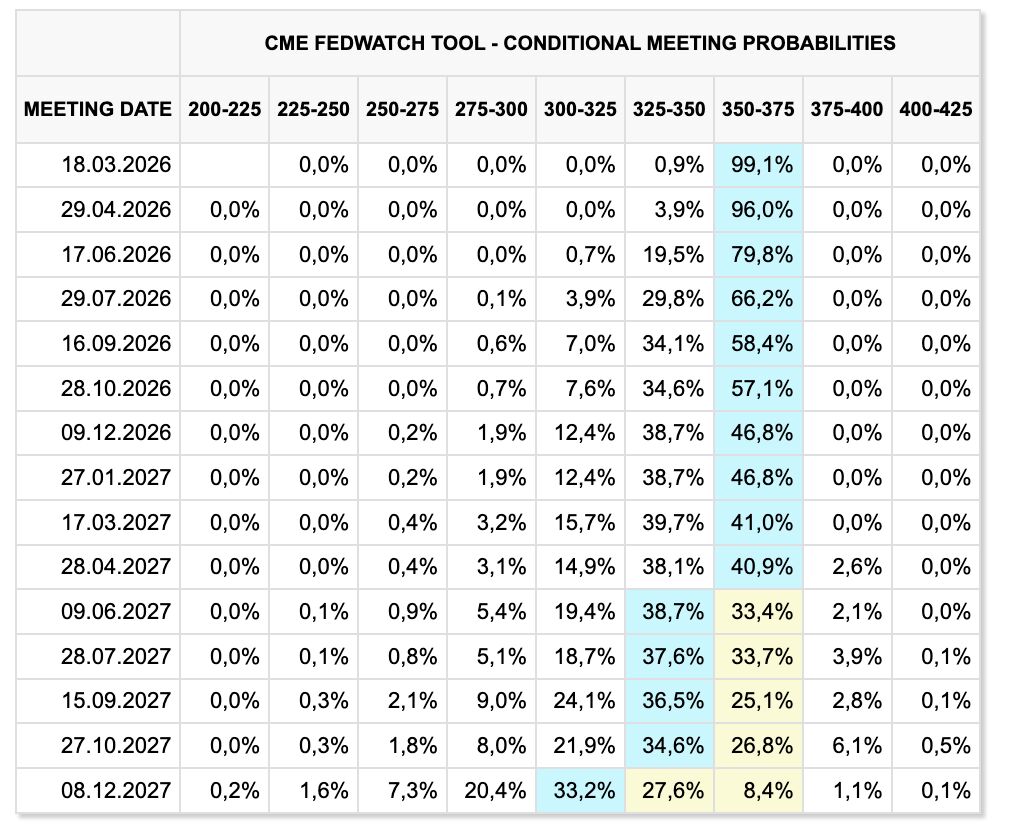

No Cuts This Year … At Least For Now!

FED Funds Futures now imply zero cuts in 2026 and only one cut in 2027 as…

-

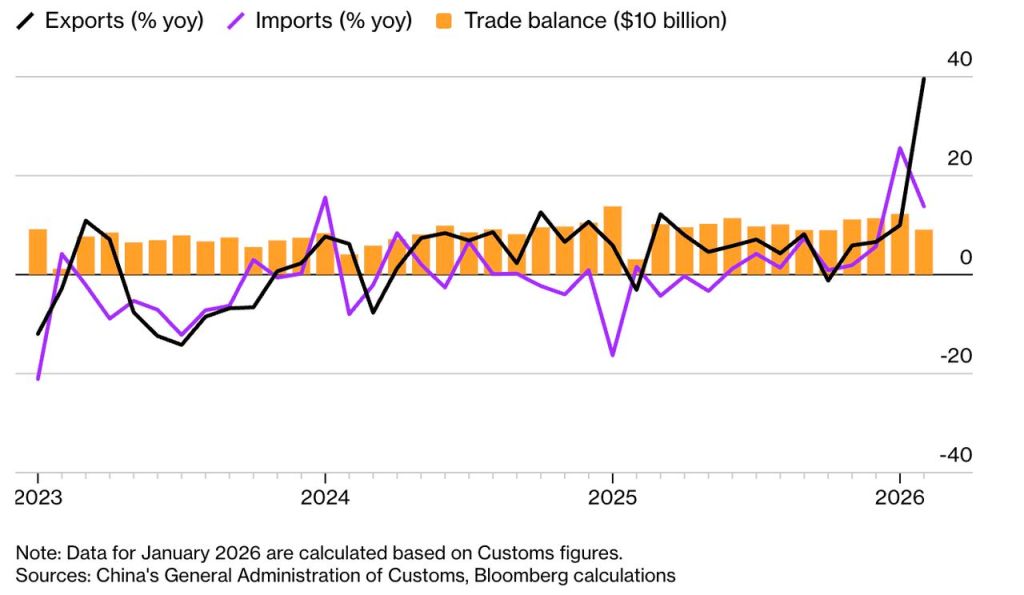

The Revival of China’s Domestic Consumption Is Unlikely. At least in 2026…

As I’ve outlined before – despite Beijing’s aim to accelerate domestic consumption and reduce overreliance on…

Independent research and commentary for informational purposes only. Not investment advice.