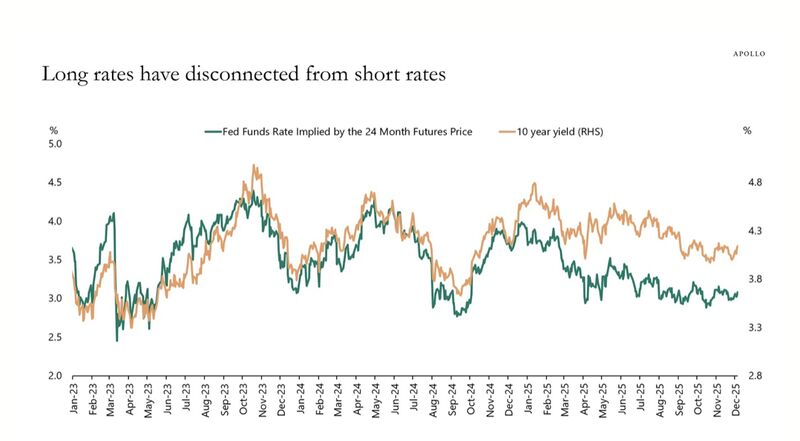

As the FED is expected to deliver a rate cut today, the divergence between long and short rates has emerged.

About a year ago, long-term yields began climbing above the levels suggested by short-term rates and oil prices. Such an upswing in long-term rates is atypical when compared with how they have historically behaved during Fed easing cycles, as the fourth chart illustrates. The yield curve keeps steepening.

It seems that now 4% is the new equilibrium risk-free compensation rate. Investors are no longer willing to hold U.S. debt for ultra-low rates and rather require a higher premium. Based on what I read and analyzed, my take is that this is primarily due to:

1. Structural budget deficit in the US

2. Geopolitical instability

3. Tariffs and trade fragmentation

4. Higher inflation volatility and expectations

5. Increasing strength of emerging markets

Leave a comment