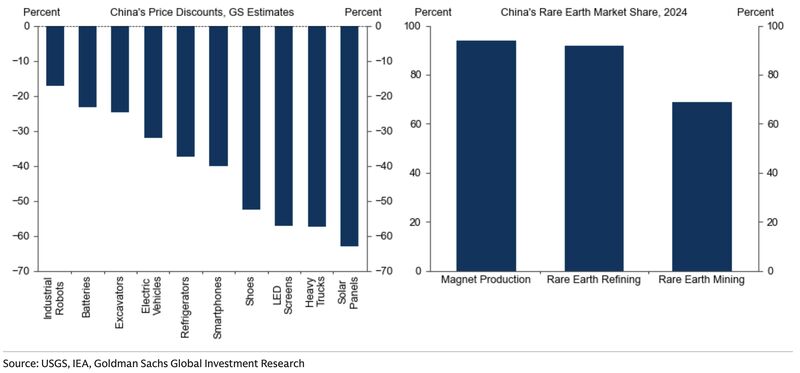

China’s export strength is increasingly structural and not cyclical. The chart shows how Chinese manufacturers can price 20–60% below global peers across EVs, batteries, solar panels, and heavy industry, which might reflect scale, integrated supply chains, and lower input costs rather than short-term dumping.

China controls the key points of the rare-earth supply chain, dominating refining and magnet production and holding a majority share in mining. That combination keeps global manufacturing deflationary, raises the cost of re-industrialization in the West, and makes protectionism an expensive and imperfect fix.

Cost leadership plus upstream control is a hard advantage to unwind.

Leave a comment