Euro-denominated bonds are now accounting for a larger share of acquisition funding than at historic levels.

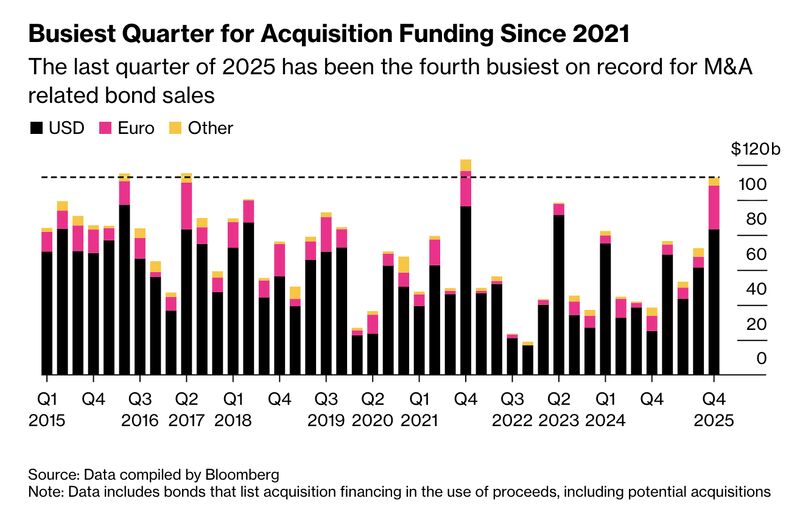

According to Bloomberg, companies are increasingly issuing bonds before M&A deals even close, locking in cheap funding while sentiment is strong. Q4 2025 became the busiest quarter for acquisition financing since 2021, with $113bn raised globally, as tight spreads and heavy investor inflows absorb supply with ease. Pharma and healthcare are leading the charge, often months ahead of deal completion and notably without paying a premium for M&A clawback clauses. In some cases, firms are even issuing without special protections, confident that the debt can be repurposed if deals fall through.

I see this as a precautionary move. With debt cheap and investors eager to buy bonds, companies are borrowing early rather than waiting for deals to close. The goal is simple here, that is to lock in attractive terms before market conditions change.

This sends mixed signals. Positively, firms are confident enough to raise debt ahead of deal certainty amid strong investor demand. On the negative side, it might mean that debt will become more expensive in the future. We already saw that in 10Y and 30Y treasuries yields are rising, and spreads between short and long duration bonds are widening.

Leave a comment