All key investment indicators in China have been experiencing a declining growth trend over the past year.

Fixed-asset investment growth: –1.7% (YTD)

Infrastructure investment growth: 0.1% (YTD)

Property investment growth: –14.9% (YTD)

Manufacturing investment growth: 2.7% (YTD)

The rate of year-to-year growth in private investment in fixed assets has been stagnating and even turning negative in China. FDI has declined as well. The level of consumption as a % of GDP also didn’t increase (about 39-40% now, while developed economies usually have ~50%), with an increase in savings and worsened consumer confidence.

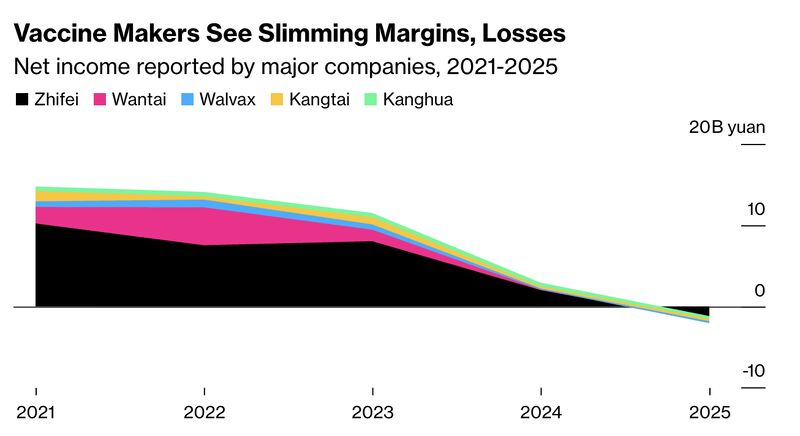

Inflation is also extremely low, which highlights both weak domestic demand and overcapacity in the economy. For example, given fierce price competition and excess supply, Chinese vaccine makers are sliding into a steep downturn, with profits collapsing, which adds yet another layer to the deflationary pressures weighing on China’s economy. Major vaccine producers have posted their first nine-month losses since listing, with some resorts to “buy one, get one free” offers and price cuts from about 150 yuan to as low as 5.5 yuan as margins collapse.

It seems that domestic consumption, private investment, manufacturing, and real estate will be the main focus for China. China is definitely on its way to self-reliance across all sectors of the economy, especially high-tech. But private investment and consumption (which are both lagging behind now in China) are extremely important for an economy to transition from a middle-income economy to a rich one.

Leave a comment