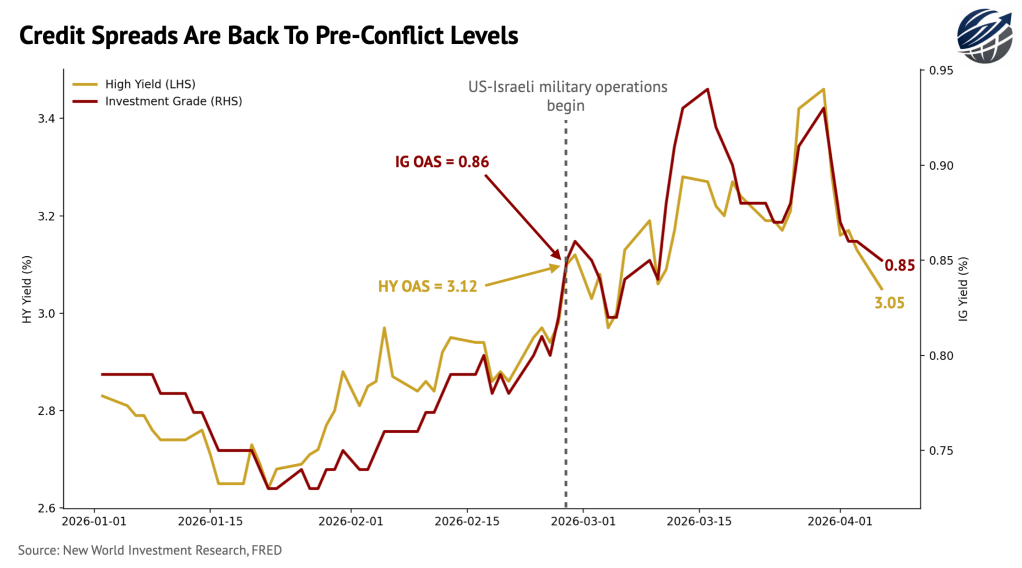

Credit spreads are back to pre-Iran conflict levels. HY OAS is back around 3.05% versus ~3.12% pre-event, and IG is near 0.85% versus ~0.86%. The widening to ~3.4% and ~0.94% was sharp but lacked persistence, with no follow-through into a second leg.

It might be that credit markets are not validating a deterioration in macro conditions. Liquidity possibly remains the primary driver, and the regime of buying spread widening is still intact. More importantly, this episode confirms that geopolitical shocks, in isolation, are insufficient to shift credit structurally wider. A spike in nonfarm payrolls in March and drop in unemployment provide some evidence for somewhat resilient demand-side in the US, but more data and time are needed to fully assess the picture.

This remains a very important theme to watch as macro conditions can swing and deteriorate quickly, which will reprice spreads in not the most favorable way.

—

Follow for more research & insights at amirkh.com

By Amir Kh.

Leave a comment