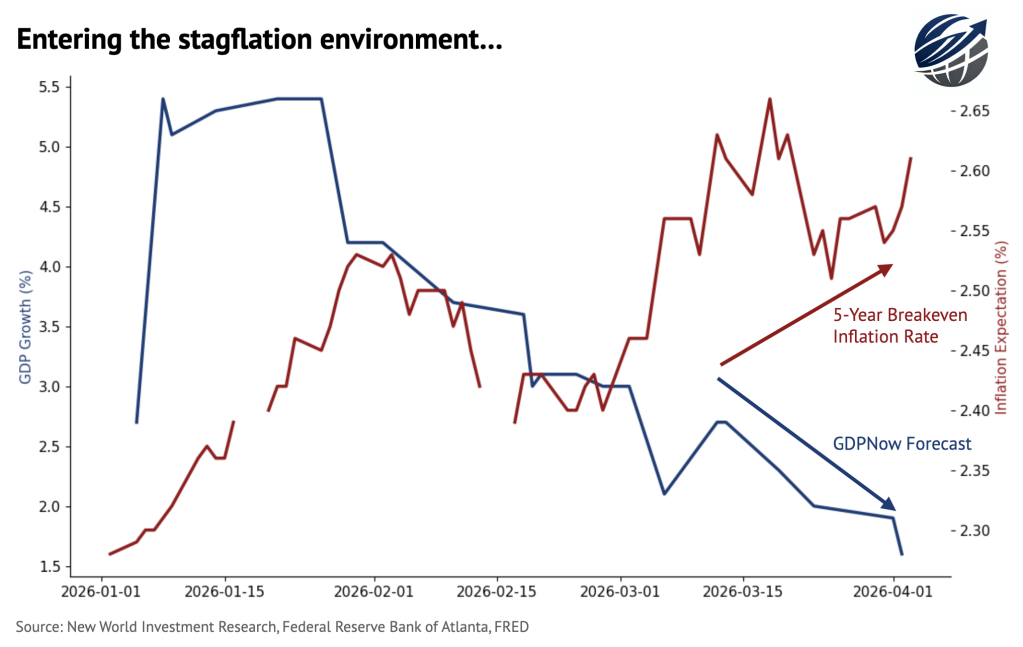

The current data from the Federal Reserve Bank of Atlanta points to lower GDP growth forecasts, while Fed data on the 5Y breakeven inflation rate shows higher expected inflation. These two trends happening at the same time perfectly coincide with the textbook definition of stagflation of low growth and high inflation, and the market signals strong worries about this.

As the conflict in the Middle East continues with no end in sight, it is important to consider the key dynamics that occurred in the most important and discussed asset classes:

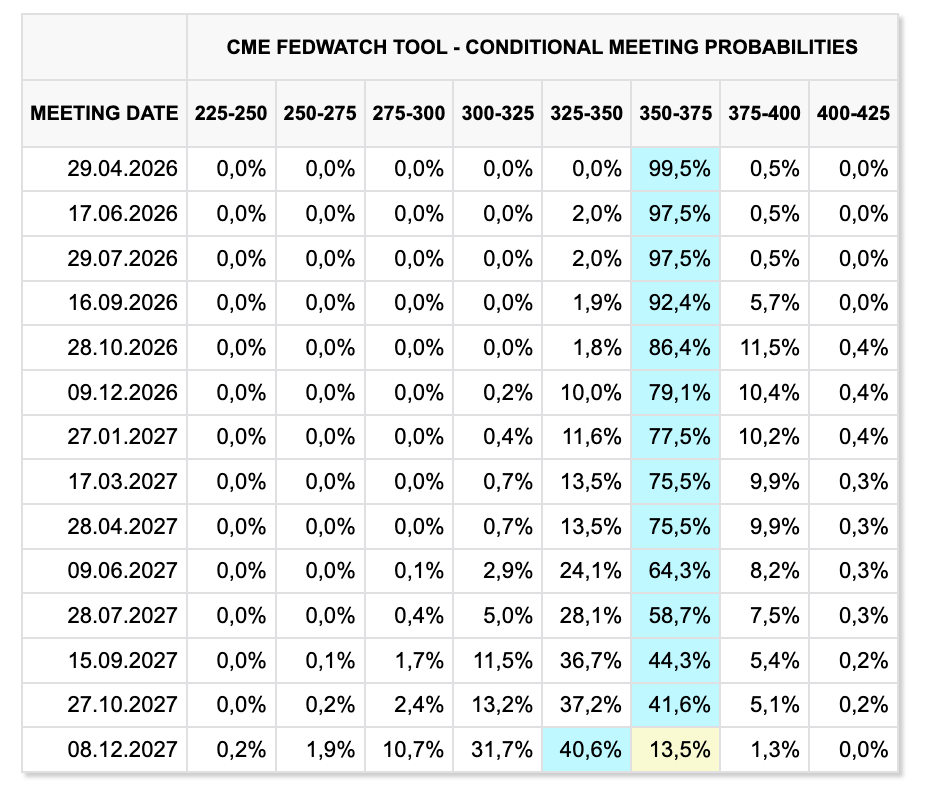

US 10Y yield: 3.97% → ~4.31%, up ~34bps. Brent above $100 repriced inflation expectations, killed the June rate cut, and the Fed explicitly flagged energy-driven price pressures at the March meeting. The 10Y is now pricing in higher-for-longer, not flight-to-safety. Futures markets are still pricing zero cuts in 2026 (Figure 2).

S&P 500: 6,879 → ~6,596, down ~4.1%. The index absorbed the worst single-week energy disruption since the 1970s and is still only in correction territory. Earnings estimates for 2026 still show +17% growth, which is keeping the floor in. The real risk is if oil stays elevated long enough to compress margins across non-energy sectors – that’s a Q2/Q3 story.

MSCI EMs (EEM): $62.58 → ~$56.52, down ~9.7%. EM had been the consensus outperformance call coming into 2026 – up 15%+ YTD at the peak in February, weak dollar, benign growth backdrop. The war blew it up. Three channels: (1) Asia’s Hormuz dependency, (2) the unwinding of crowded Korea/Taiwan tech longs, (3) dollar strength, which mechanically compresses EM returns in USD terms. MSCI EM erased its entire YTD gain by the end of March. The EAFE is down ~10%, EM down ~13% for March alone. Latin America is the relative winner within EM given commodity exposure, but it’s a relative story as absolute returns are still negative.

DXY: ~97.9 → ~99.9, up ~2%. The dollar did what it always does in a global shock, it strengthened.

Bitcoin: ~$65,572 → ~$69,747, up ~6.4%. The one asset that has outperformed its pre-war level.

Gold: ~$5,296 → ~$4,700, down ~11.3%. Gold had rallied 24% in the 30 days before the strikes, and the expectation was that an actual shooting war would send it through $6,000. Instead, it’s had its worst month since October 2008. Three forces: (1) dollar strength, as gold is priced in USD, and a 2-point DXY move creates an immediate headwind for non-dollar buyers; (2) yield repricing, where real yields rising as inflation expectations outrun nominal growth expectations makes the opportunity cost of holding a zero-yield asset painful; (3) forced selling with central banks in energy-importing EMs has been rumored to be liquidating gold reserves to raise cash for currency defense and energy imports. The ETF outflows have been massive, with billions leaving GLD in single-day redemptions. Gold came into this war overowned and overpriced relative to its fundamentals, and the war ironically triggered the unwind rather than the bid.

As the end of the conflict is nowhere near and the Strait of Hormuz remains effectively closed, the investors’ playbook is gradually turning towards degrading the environment with both inflation upside and growth downside. Markets should expect Brent oil to trade at $150 per barrel for “paper” oil and as high as $200-$250 for real delivery. These prices are abnormally destructive and undermining in nature for all countries without exceptions, which slows down global economic growth and spikes inflation. As noted before, should the conflict end tomorrow, its consequences will still be felt for at least 6-18 months, as it will take years to restore pre-conflict capacities. Moreover, with a higher risk premium in the Middle East region, from now on, investors will be more cautious on investments in the region, meaning that some pre-conflict facilities might not be restored whatsoever. Air travel, goods delivery, food, AI, centers, infrastructures, and machinery & equipment construction are just some of the industries (which are the most vital for everyday economic activity) that are severely impacted by the conflict, and markets are yet to fully realize it. Finally, as the pre-conflict growth upside and tailwinds remain somewhat robust, it is likely that markets and economies will firstly be hit by inflation pressures and later by demand destructions, meaning that for now the best policy for the Fed is to hold rates…

—

Follow for more research & insights at amirkh.com

New World Investment Research

By Amir Kh.

Leave a comment