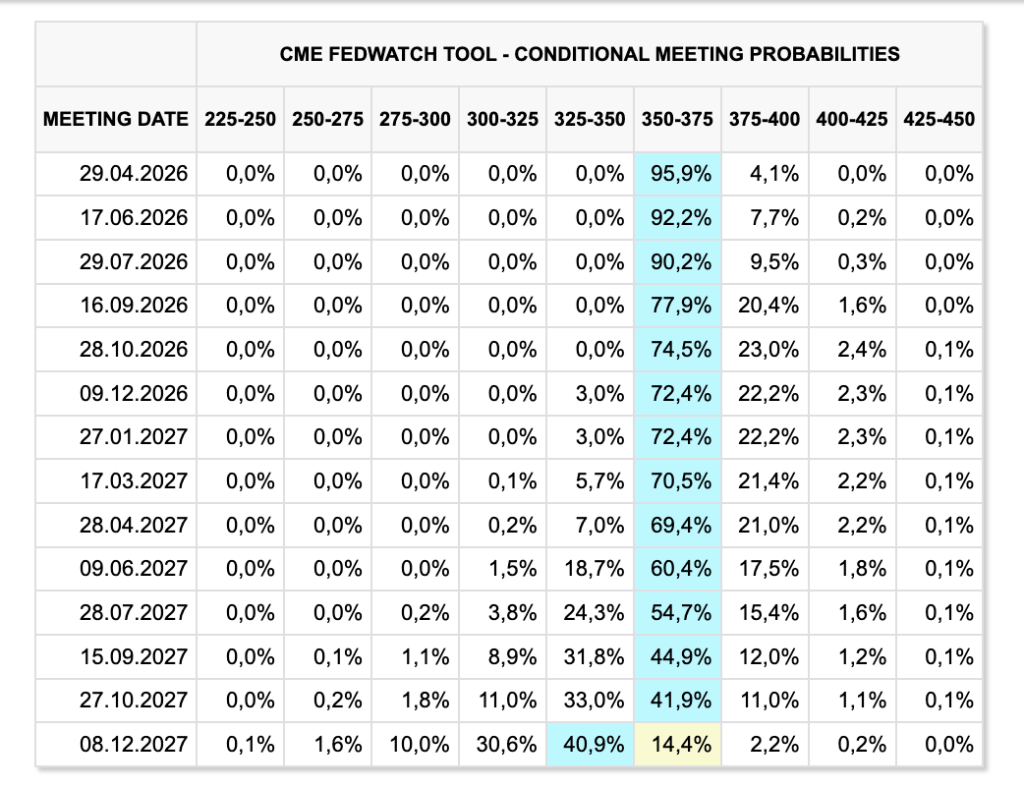

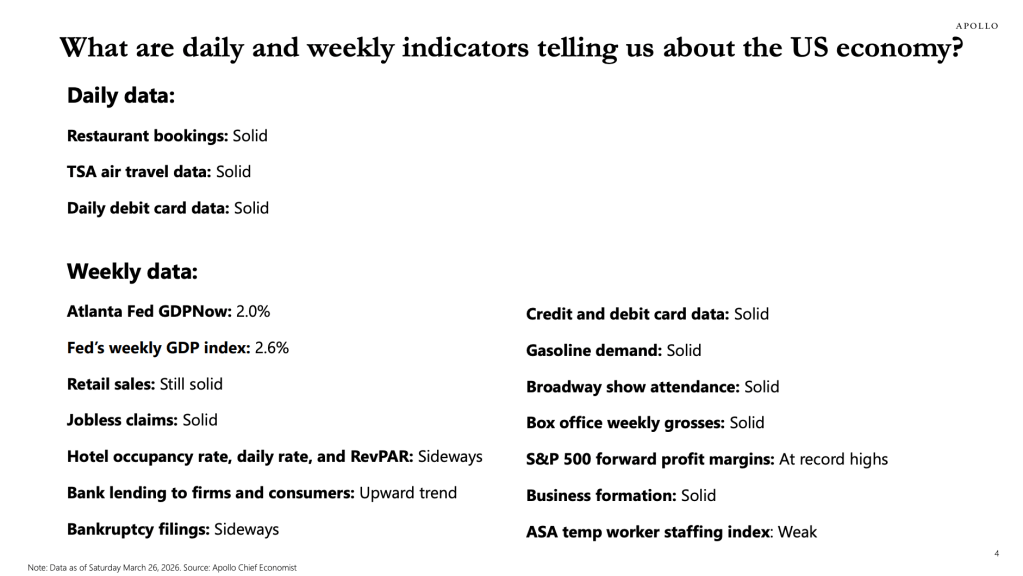

As markets are pricing higher inflation, disruptions in supply chains, and widening energy shortages, central banks over the globe are aligning towards holding or hiking rates. The Fed is not an exception. Fed Fund Futures imply steady rates for 2026 and one cut in 2027 as late as December (Figure 1). Some traders are wagering on Fed hikes even in this year. Although my view is that the conflict will be far more prolonged (than the market currently prices in) with extremely deteriorating and undermining consequences for energy and food markets for the next 12-24 months, meaning that demand deconstructions might outweigh inflation concerns and implying no changes to the rates, there are reasonable arguments for a more hawkish stance. As such, recent Apollo data provides strong evidence for the persistency and robustness of tailwinds for US growth (Figure 2).

As of now, the Iran shock is not big enough to offset the strong tailwinds to the US economy from AI spending, the industrial renaissance, and the One Big Beautiful Bill. However, this is very conditional on how conflict will continue to evolve and, more importantly, how it will shape macroeconomic indicators of the United States and other economies. My take is that demand deconstructions will become more prominent near early May in the US among consumer discretionaries, construction, travel, and other industries that are sensitive to fuel, energy, and food prices.

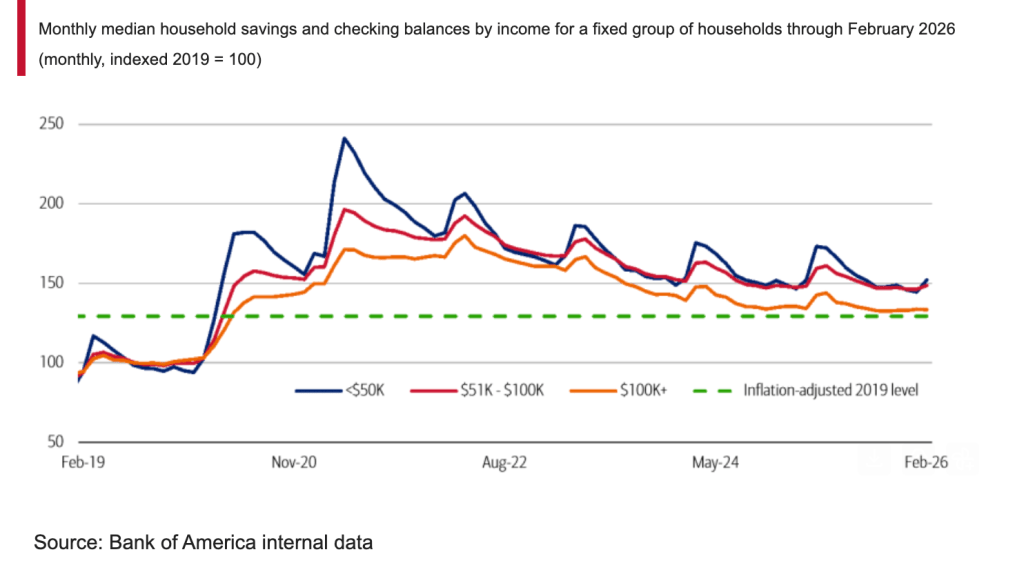

Moreover, since the US economy is K-shaped in nature (see my earlier note on this), the growth in the US will be skewed even more towards AI-related industries, while everything else will see stagnation and recession. Higher energy prices will not hit the US economy immediately, but likely to do so around May-June since median checking and savings deposit balances remained above inflation-adjusted 2019 levels, providing additional cushion for households (Figure 3). Therefore, it all depends on when and how the conflict will be resolved. However, should it all stop tomorrow, the negative impacts will still be there for around the next 6-18 months, meaning that inflation is the key issue for policymakers in 2026 and 2027 for sure. The demand side that was driving the US growth before the Iran war (CapEx, Fiscal Spending, AI) seems to be relatively more resilient and will experience rather short-term fluctuations and possible slowdowns rather than complete demolishment.

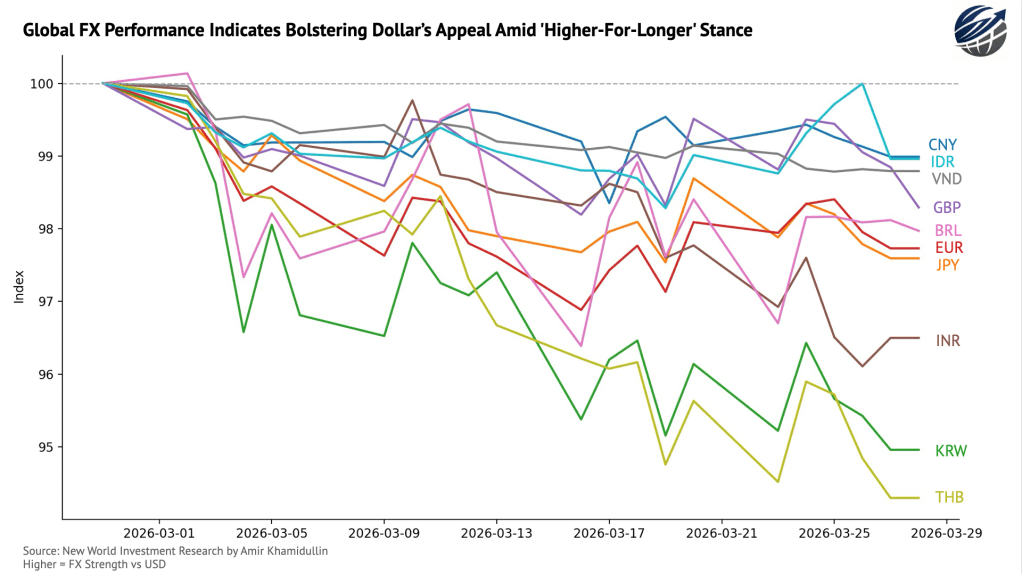

The striking feature of this conflict is FX performance. All major currencies depreciated against the dollar since the outbreak of the conflict in the Middle East (Figure 4). In other words, the dollar is back. Its safe-haven appeal, ‘higher-for-longer’ policy expectation, and disruptions in other nations that were actually outperforming the greenback before the conflict are attracting more capital. from investors.

The government bonds, however, are obviously not so happy with energy shocks and inflation fears. Yields in almost all key economies surged since February 27. Furthermore, as I mentioned before, since most nations in EMs are net energy importers, investors are rotating away from EMs amid growth and stagflation fears. As their currency depreciates, EM countries will see their current account deficits widening, growth compressing, credit conditions tightening, and inflation spiking. This is definitely contractionary for these economies, but not structural. In other words, while development and growth will be suppressed in emerging markets for the next 6-18 months, the fundamental position with which they entered 2026 is still present. Corporate earnings, investments, R&D, and other fundamentals that are structural in nature are very unlikely to be undermined and deteriorated in a way severe enough to completely rewrite the 3-5 year macro case of these nations.

—

Follow for more research & insights at amirkh.com

By Amir Khamidullin

New World Investment Research

Leave a comment