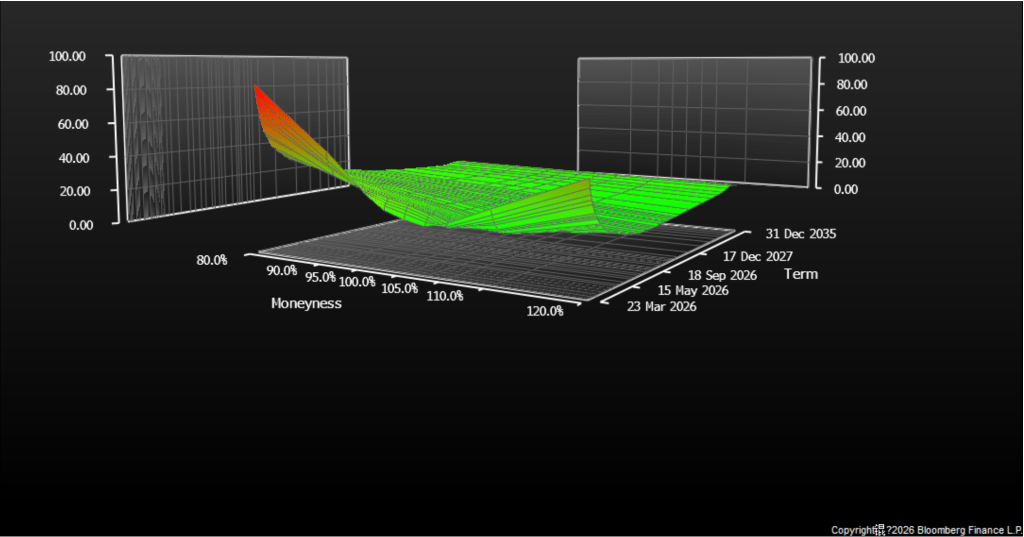

The S&P 500 implied volatility surface gives some interesting observations.

Near-term put skew spiking to 80-100 vol at 80-90% moneyness means the market is actively pricing a further 15-20% drawdown by mid-2026 and in the current macro context that’s definitely not noise. ATM vol is moderate, and the call surface is flat dead, so there’s relatively little bid for upside. It seems that the market has a rather consolidated view.

In other words, left-tail vega is being bid to extremes while call-side vega is entirely flat, confirming the market has a singular directional view with no premium being assigned to upside scenarios. The gamma concentration in short-dated OTM puts reflects acute near-term fear rather than structural long-term repricing, which is supported by the term structure where back-end vega is compressed and flat, meaning the market sees this as a 2026-specific dislocation, not a regime change.

The bottom line is that the market should expect increased turbulence and possible downturns in S&P500 in the coming months, but the structural foundations and valuations in macroeconomics, investment, CapEX, AI are still supportive for broader growth of the economy and equities.

#options #spx #volatility

—

Chart Source: Bloomberg

Follow for more research & insights at amirkh.com

New World Investment Research

Leave a comment