As the conflict in Iran unwinds further with deeper escalations happening on a daily basis, it seems that markets and politicians are underestimating the ongoing dynamics and deteriorating consequences they are already having for the world and, most importantly, will have later.

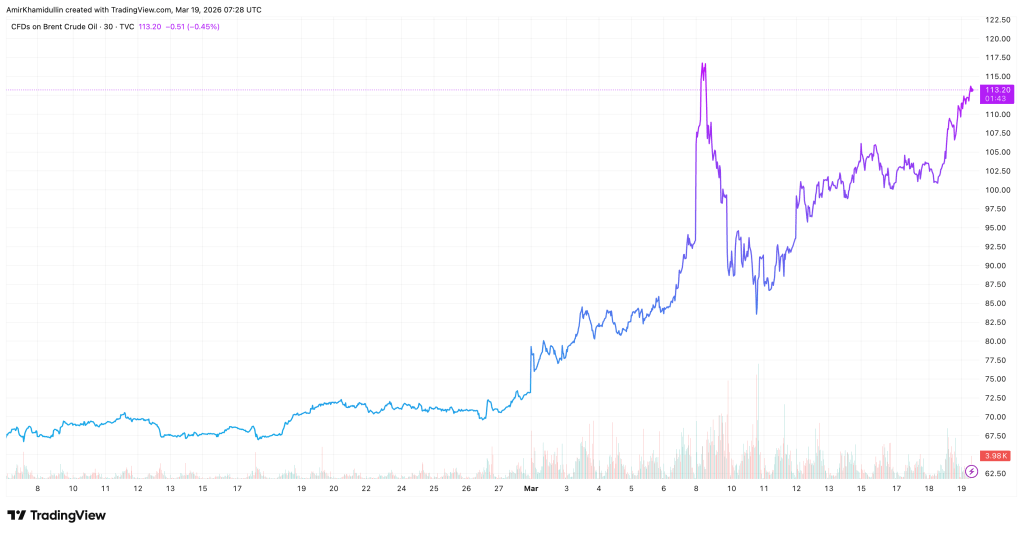

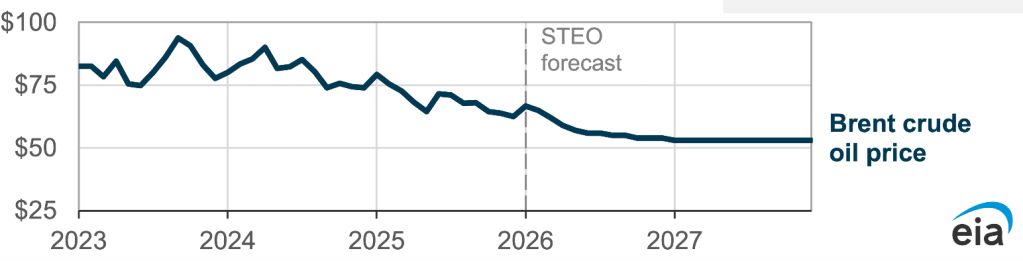

At the time of writing this note, futures on Brent oil are trading about 60% above pre-Iran conflict levels at around $113 per barrel (Figure 1). For reference, the Congressional Budget Office (CBO) and the Office of Management and Budget (OMB) in the United States were projecting Brent crude to average approximately $58 – $60 per barrel for 2026, assuming a global supply surplus (Figure 2). While China’s energy assumptions are less transparent, they are heavily tied to the 15th Five-Year Plan (2026–2030), which was released in early March 2026. The National Development and Reform Commission (NDRC) generally bases its industrial planning on a “stable range” of $60 – $70 per barrel. This factor alone puts pressure on two of the world’s major economies, costs of production, and inflation.

Source: TradingView, New World Investment Research

Source: U.S. Energy Information Administration, EIA

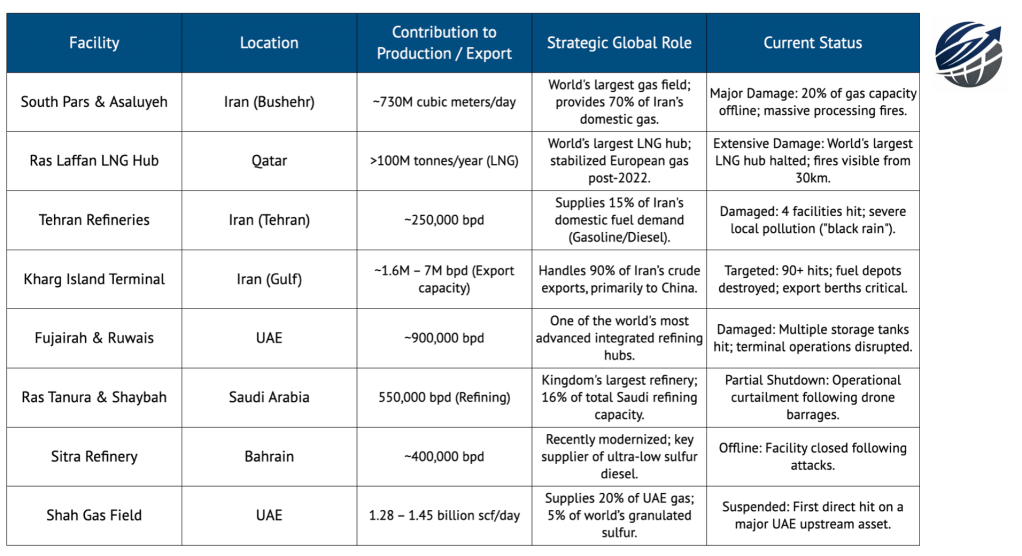

To more precisely value the impact of energy flow disruptions on the world and market, let’s consider which gas & oil production facilities have already been damaged or destroyed. Not to mention effective closure of the Strait of Hormuz since February 28, some of the world’s most important and advanced oil & gas refineries and production sites located in the Middle East and Iran have been severely damaged. Figure 3 includes only a selected number of facilities attacked that were publicly reported and that are having the most prominent impact on energy. This is far from being the complete list. As a result of military actions, these production facilities are attacked daily, meaning that every single day of the conflict imposes more and more risks on widening and persistent shortages for the global energy flows, with energy-importing countries suffering the most. IRGC recently claimed that Iran will “burn down” its entire energy infrastructure in response to attacks on Iranian oil facilities. Therefore, with no end to the US-Israel-Iran war in sight (which I will explore below as well), it seems that the current oil and gas prices underestimate the severity of the crisis. Markets should expect oil prices to stay well above $130 per barrel levels and even reach levels of $160-$170 per barrel. Citadel’s bimodal probability distribution model predicts oil trading either around $70 or closer to $150. Importantly, should the conflict come to an end soon (which again seems extremely unlikely due to the reasons I will explore below) and Strait of Hormuz to open, the restoration of these facilities would not be a simple “flip of the switch” because these sites involve high-pressure systems, volatile chemicals, and specialized global supply chains. It will take ~3-12+ months to restore the pre-conflict capacities and productivity levels, depending on the extent of the damage, which is already enough to have very painful effects for energy markets and global economic growth (given that attacks are over!!!).

Source: New World Investment Research, The National News, Farmonaut, Hellenic Shipping News Worldwide

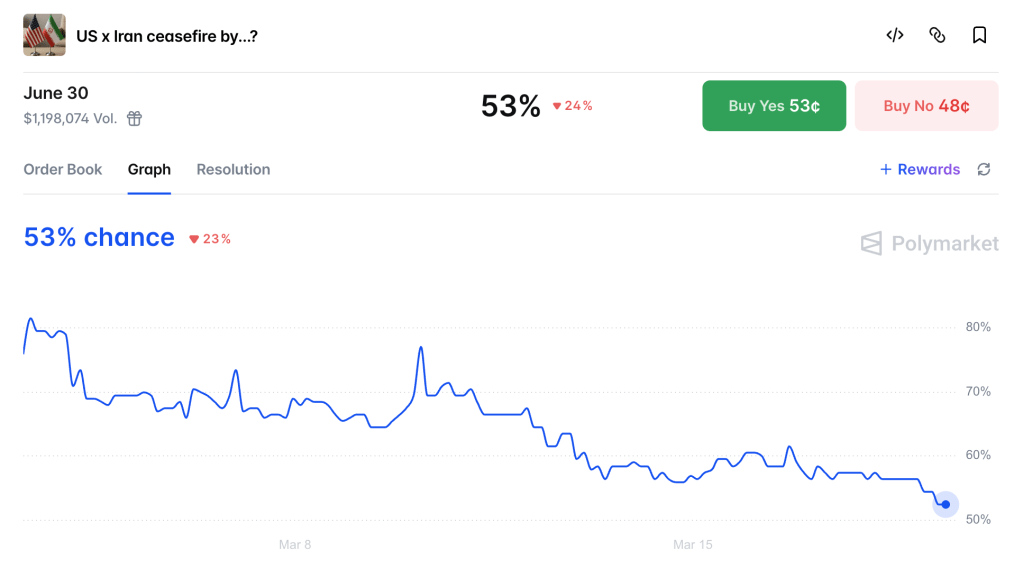

Polymarket currently gives about a 53% chance of a ceasefire by June 30 (Figure 4). Even if the ceasefire indeed occurs by June 30 and the Strait of Hormuz opens, tankers pass through and reconstruction of production sites in the Middle East begins (which will take 3-12+ months to complete), oil & gas prices will still be elevated far above benign equilibrium levels needed for normal and complete functioning of the global economy.

Source: Polymarket

Therefore, the current market’s pricing and estimations appear to dangerously undervalue the real risks of the conflict, as a ceasefire by June 30 still seems very unlikely for a number of reasons. First, Trump’s administration’s mixed rhetoric on aims and actions (ranging from the conflict being over in days and weeks and even months as well as from Iran’s military being completely destroyed to Iran showing notable resistance) regarding military operations in Iran gives feelings of their own uncertainty and unclarity on how to proceed next. Second, even if troops are deployed on the ground, it is unlikely to get the conflict closer to the end given extremely hot temperatures in Iran in the summer, mountainous geographics, and political complexity in sending U.S. soldiers. Third, the cost-effectiveness of strikes seems to be on Iran’s side with relatively cheap drones (~$30,000 each) versus extremely expensive and high-tech missile systems (Tomahawks at $3.6 million each). Finally, we should remember that for Iran this war is a fight for survival and national independence, meaning that there is basically nothing to lose for Iran, and likely they will fight till the end with an ‘all-in’ mindset.

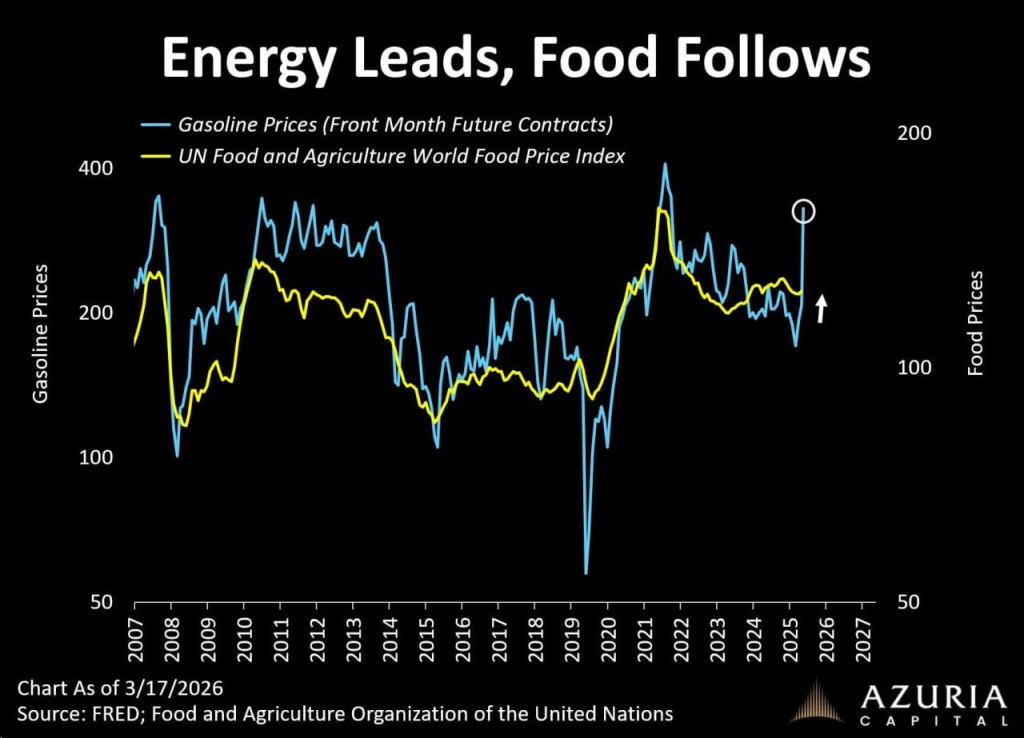

Another risk that is being somewhat underlooked by the media, politicians, and general public is food prices. The Strait of Hormuz is the world’s most critical artery for fertilizers. Roughly 25% to 30% of global nitrogen fertilizer exports pass through this narrow waterway. Moreover, nitrogen fertilizer is made from ammonia, which requires natural gas. As the conflict has sent global LNG (liquefied natural gas) prices up by over 50-70%, the cost of manufacturing fertilizer in the U.S., Europe, and Asia has also skyrocketed. The timing is particularly damaging for the Northern Hemisphere, as the conflict began just as the spring planting season was kicking off. If farmers apply less fertilizer to save on costs, crop yields (the amount of food produced per acre) will drop. Experts warn that even a modest reduction in nitrogen use can lead to disproportionately large declines in the global harvest. In other words, the world and fertilizer and nitrogen-importing countries should prepare for higher food inflation and possible shortages. The historic link of agricultural and gasoline prices provides further evidence for food prices’ upside (Figure 5). This is an immediate risk as it will target the lives of every single household in dependent countries.

Source: Azuria Capital

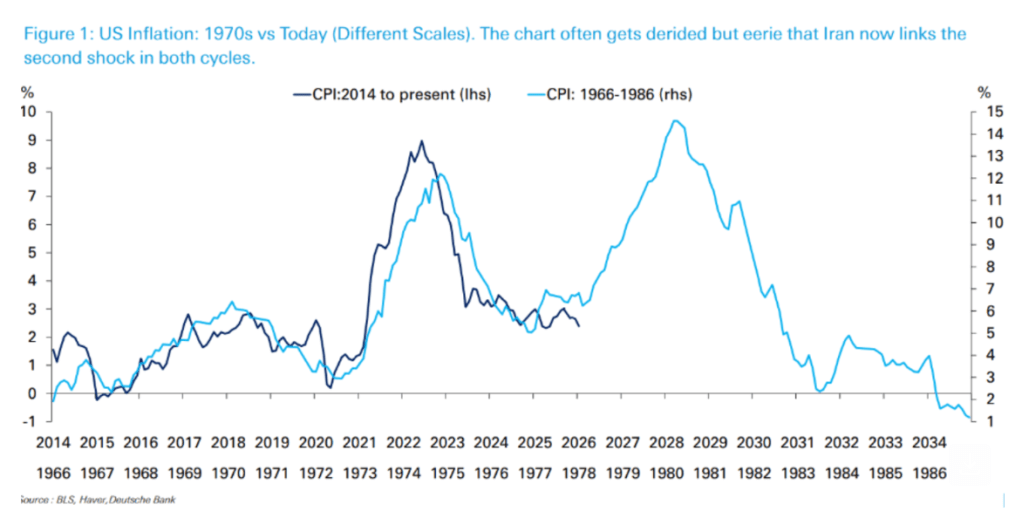

With pre-Iran inflation rates running already above the 2% target and the most recent PPI reading coming at +3.4% YoY (est. +2.9%) in the U.S., the Fed is in a very tough position along with other central banks across the world. As I reiterated previously many times, even before the outbreak of war in Iran, the combination of large fiscal stimulus, very loose monetary conditions, extremely low credit spreads, reduced migration, and lagged effects of tariffs was already exerting upwards pressure on inflation in the U.S. The ongoing conflict will undoubtedly add to the existing trends and put inflation well above current 2.4%. I am expecting it to be around 3.0% by the end of 2026. On top of that, the parallel between the 1970s vs. today is still worth watching, given how shockingly similar CPI trends already have been (Figure 6).

Source: Deutsche Bank, Bloomberg

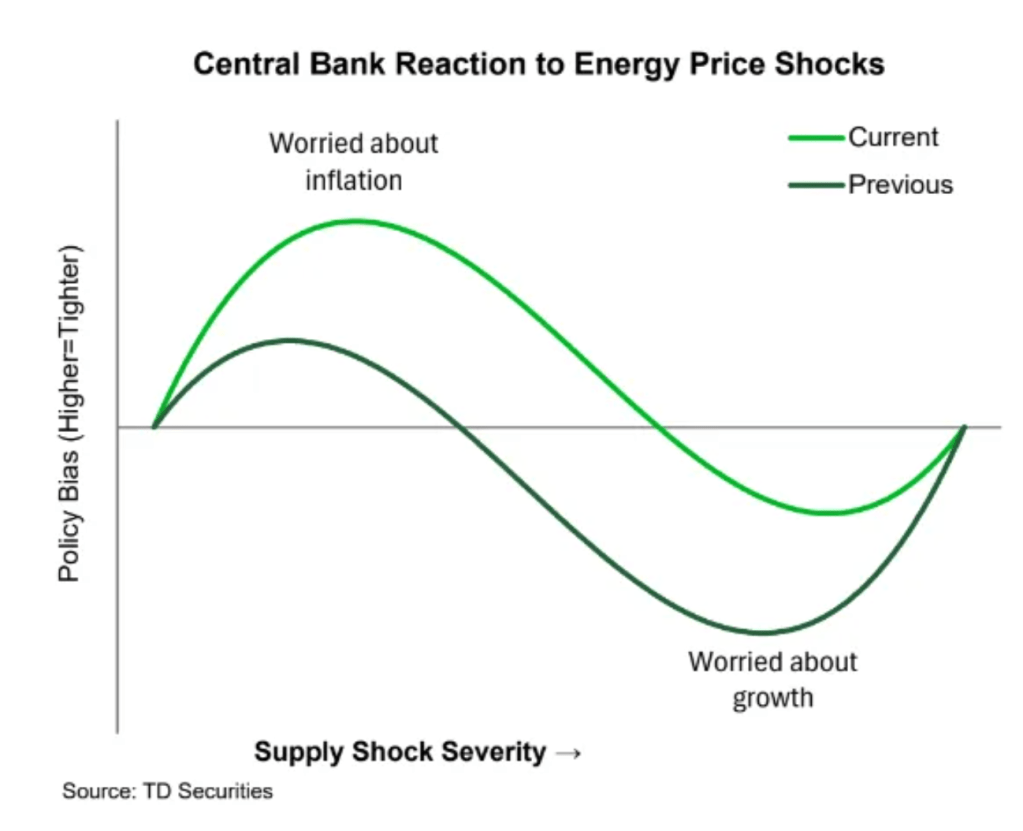

Moreover, as central banks across the world are deciding on their policy trajectories given energy supply shocks and resulting inflation pressures, it is important to be vigilant on how spikes in gas & oil prices do not only lead to supply shocks but also impact the demand side of the economy (Figure 7).

At a certain point, demand destruction begins to outweigh inflation concerns, implying a more dovish monetary stance despite traditional rate hikes’ response to supply shocks.

Source: TD Securities

It is also possible that, historically, higher energy prices followed by recession periods were not driven purely by stagnation and fall in households’ purchasing power, consumption, and investment, but rather by overly tightening monetary policy in which rates were put too high – further supressing demand and growth.

So the question is, should central banks cut rates rather than hike them if energy prices’ elevation is persistent enough to pass through the economy and undermine demand? If so, how to determine the extent of persistence and when regulators should ease monetary policy?

All in all:

1) Energy shock is structural, not temporary

Oil prices far above pre-conflict assumptions reflect real supply disruption (damaged infrastructure + Strait of Hormuz constraints). Even with a ceasefire, recovery takes months, meaning elevated energy prices are likely to persist and keep production costs high globally.

2) Second-round effects → food inflation & global pressure

Higher gas prices raise fertilizer costs, reducing agricultural output and pushing food prices up. This extends the shock from energy into everyday consumption, increasing inflationary pressure and hitting households directly.

3) Central banks face a stagflation dilemma

They must choose between fighting inflation (rate hikes) and supporting weakening demand (rate cuts). The key risk is overtightening into a supply shock, which could trigger recession – making this environment increasingly resemble a stagflation scenario.

This note is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. The views expressed reflect the authors’ judgment as of publication and may change without notice. Information is believed to be reliable but is not guaranteed for accuracy or completeness. Past performance is not indicative of future results. The authors or affiliated entities may hold positions in the securities discussed. Recipients should consider their own financial circumstances and consult professional advisors before making investment decisions.

Leave a comment