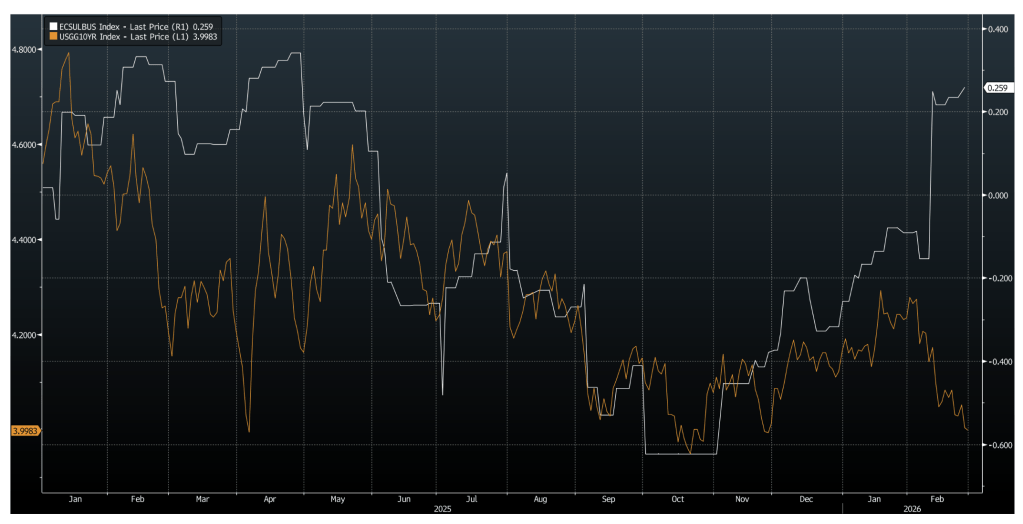

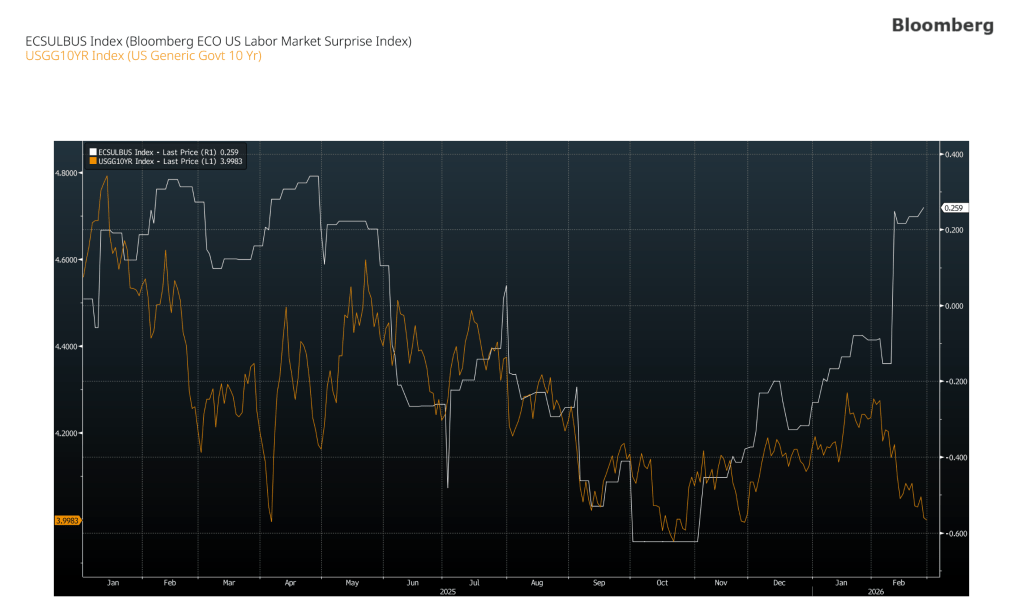

Yields are lagging behind and diverging away from the ongoing macroeconomics backdrop. The Bloomberg US labor market surprise index spiked from -0.16 to 0.26 since the beginning of February, while the yield on 10Y Treasuries continued its downward trend.

Recent labor data, stronger-than-expected payroll growth, and improving participation support the narrative of a firming economy. PMIs and corporate earnings trends also indicate ongoing expansion rather than a slowdown.

If equities continue to advance while yields remain contained, overall financial conditions would ease further despite solid growth. That kind of divergence typically creates a structural imbalance, which shouldn’t persist for long.

However, treasuries are still demanded by both local and international investors. The global outlook must also be considered since the Fed anchors the front end of the yield curve, while the rest of the curve is determined by global demand, risks, etc. The easing fiscal and inflationary pressures in Japan, amid Takaichi’s election, might partly explain why 10Y yields are at the lowest point since November given the firm and hot growth outlook in the US.

Many factors are definitely at play here, and some of those can’t be observed and quantified.

Leave a comment