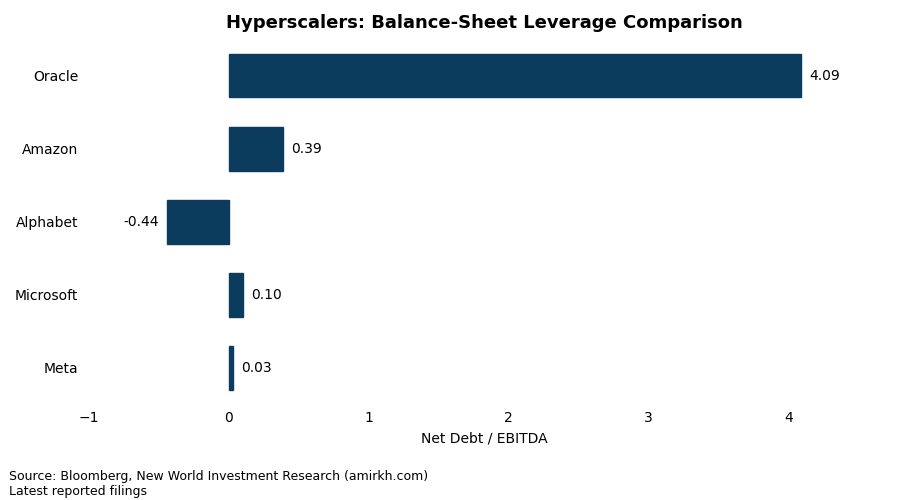

The divergence in Net Debt / EBITDA across hyperscalers maps directly into credit OAS dispersion. Microsoft, Meta, and Alphabet, with net leverage near zero or negative, trade at tightly compressed spreads, reflecting minimal balance-sheet risk and ample capacity to self-fund AI capex; for these issuers, AI investment requires little to no additional spread compensation. Amazon sits in the middle since AI capex is partly debt-funded, but improving EBITDA has kept leverage and OAS contained.

With Net Debt / EBITDA around 4x, AI expansion is being financed through leverage rather than cash flow for Oracle, and this is reflected in a structurally wider OAS versus peers. More broadly, the AI build-out – nearly $600bn of hyperscaler capex expected in 2026, up ~45% YoY – has not translated into systemic credit stress. Most high-grade tech bonds trade at ~50 bps or less, with short-dated issues in some cases near zero or negative spreads, leaving limited carry but also limited volatility.

If AI capex fails to translate into durable revenue and cash flow, even today’s fortress balance sheets could face pressure, particularly for issuers leaning more on debt.

Leave a comment