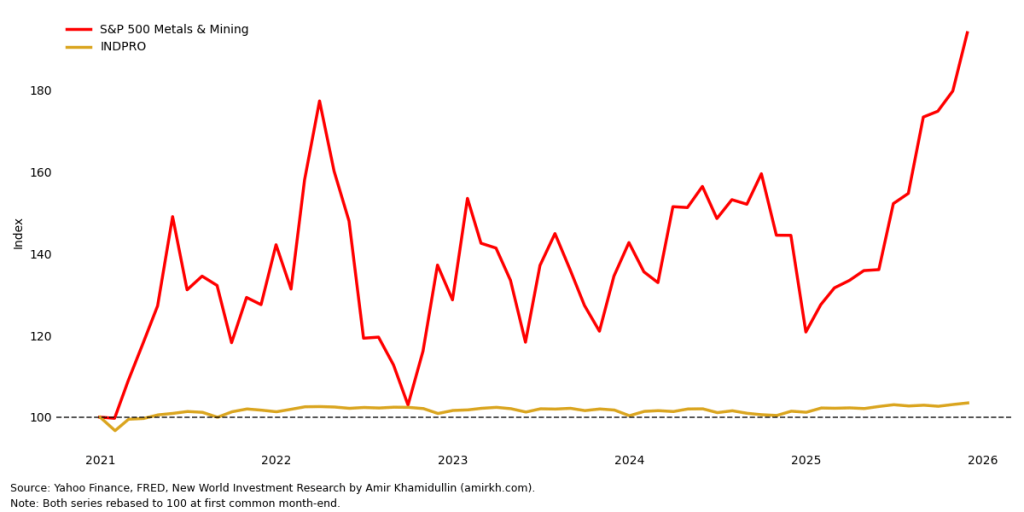

While the S&P 500 Metals & Mining index has increased by over 80% since 2020, the industrial production index has yielded little to no return. It implies that the valuation of metals and mining equities is mainly driven by expectations of future earnings and tightening supply rather than by a meaningful increase in current U.S. industrial metal consumption.

In this sense, the sector is behaving less like a proxy for U.S. manufacturing activity and more like a high-beta expression of reflation and commodity super-cycle expectations. Absent a sustained acceleration in industrial production or other real-activity indicators, this valuation gap increases the risk of mean reversion should expectations fail to materialize.

#commodities #usa

Leave a comment