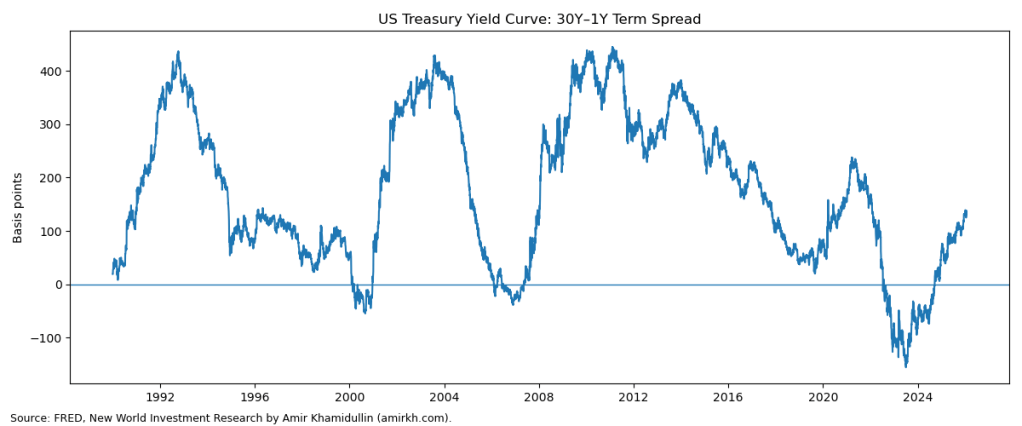

The term spread between yields in 30Y and 1Y treasuries is rising, resulting in a “bull” steepening of the yield curve. The trend is driven by a fall in 1Y yields while 30Y ones stay relatively calm, which implies market expectation of further rate cuts, but the magnitude of easing in monetary policy is unclear given mixed labor market and inflation signals. The FED Fund Futures rates for 2026 also support this view.

Historically, as per the chart, reversion from near-zero levels in term spread lasts for an extended period of time and reaches the 300-400 bp level at the peak. Given that the downside for 1Y yields is very limited in the US (due to high inflationary expectations for 2026 and other macroeconomic factors) and if the reversion trend takes place this time as well, then we might expect a rise in long-dated yields, driven by rising term premia rather than policy expectations.

This is consistent with the ongoing dynamics in the market: weakening dollar, reduced exposure to US debt by foreign holders, diversification from the US market, higher debt, and geopolitics.

—

Follow for more at amirkh.com

Leave a comment