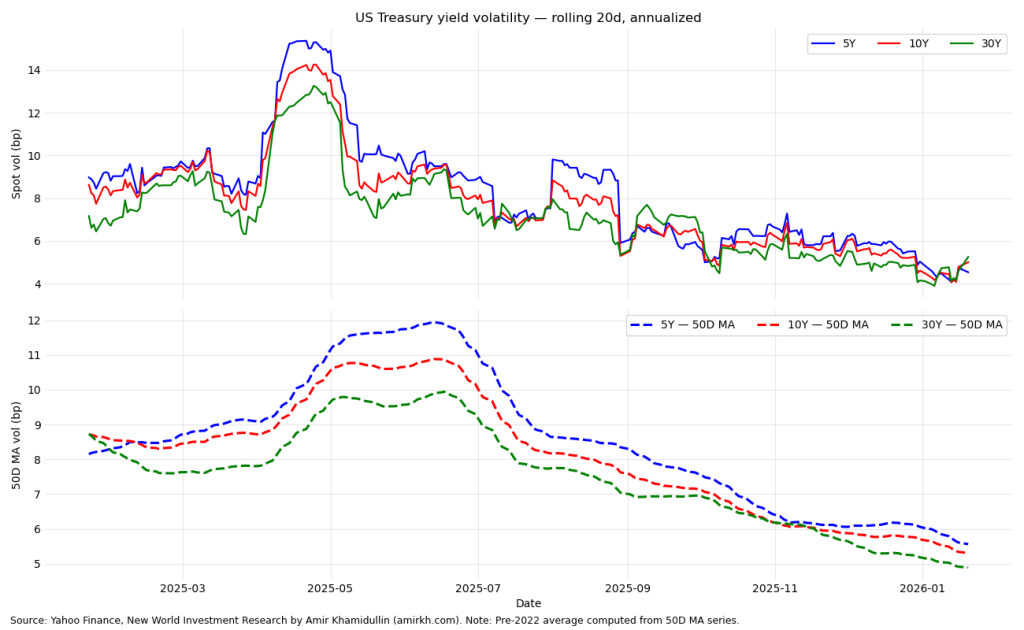

US Treasury yield volatility has declined materially across the curve over the past year. Rolling 20-day volatility in 5Y, 10Y, and 30Y yields peaked in spring 2025 and has since trended lower, with current levels near the bottom of the post-pandemic range. The decline is visible both in spot volatility and in the 50-day moving average, indicating a sustained regime shift rather than short-term noise.

The compression in US Treasury yield volatility suggests that tariff-related uncertainty is largely priced in by the rates market. Despite ongoing policy and geopolitical noise, volatility across the curve has fallen below pre-2022 norms, indicating that investors no longer view tariffs as a regime-changing risk for inflation or the Fed’s reaction function. Instead, tariff risks appear to be treated as manageable-level effects, with limited implications for long-term rates unless policy escalates in a nonlinear way.

#us #yields

Leave a comment