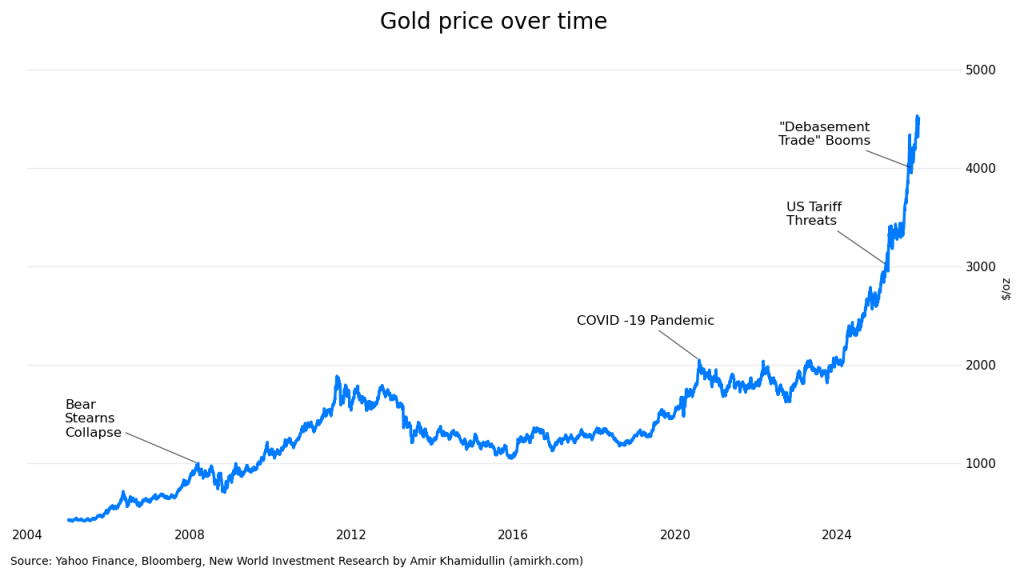

The previous year concentrated nearly all of the conditions that traditionally support gold: declining interest rates, elevated geopolitical risk, a weaker dollar, trade restrictions such as the “Liberation Day” tariffs, and increased speculative activity from retail investors. As Bloomberg notes, swelling public debt in advanced economies intensified political tensions, from budget standoffs in the United States to fiscal paralysis in France and scrutiny of Japan’s record deficit under new leadership.

In 2026, these factors are unlikely to reverse, but they may lose momentum. Rate cuts are increasingly priced in, the dollar’s weakness may stabilize, and speculative demand tends to fade once the initial repricing is complete. As a result, gold’s performance is likely to depend less on short-term shocks and more on structural demand, particularly from central banks and long-term institutional investors.

The underlying macro backdrop remains supportive, but the scale of gains seen in 2025 set a high base. Going forward, gold is more likely to act as a portfolio stabilizer and store of value rather than a source of outsized returns.

#gold

Leave a comment