LNG imports, particularly from the U.S. (now a key supplier to Europe), remain structurally more expensive than pipeline gas from Russia. In 2024, U.S. LNG delivered to Europe averaged around $15/MMBtu (≈50 €/MWh), while spot prices at European hubs such as the Dutch TTF traded mostly in the 30–45 €/MWh range in early 2025.

Europe’s post-2022 shift from Russian pipeline gas to LNG therefore raised industrial energy costs materially. Before 2022, Russian pipeline gas via routes such as Nord Stream was often 30–50% cheaper than U.S. LNG, and this differential has largely persisted into 2025. Some market estimates point to Russian gas prices near €11/MWh, compared with LNG-linked TTF prices closer to €40+/MWh, though such figures vary by contract and timing. By contrast, China continues to benefit from lower-priced Russian pipeline gas, with 2025 projections near $8/MMBtu, versus $10–12/MMBtu for LNG imports.

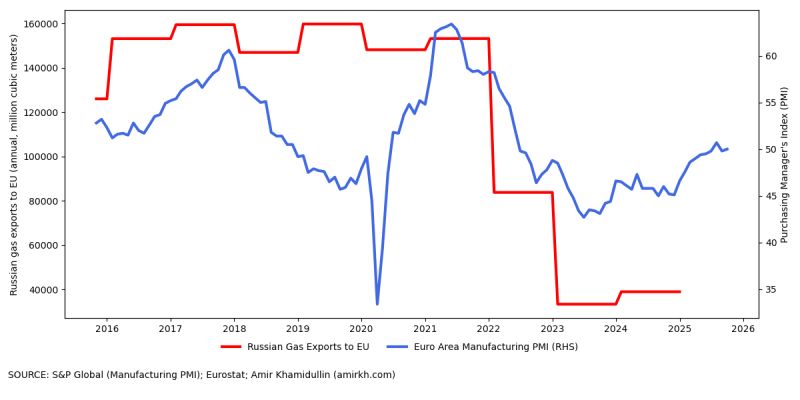

This trend is evident in the chart, as PMI dropped from 60 to below 50 levels since 2022, which indicates contraction rather than growth in European manufacturing. The fall in PMI is consistent with the sharp decline in imports of gas from Russia.

Increasing competition from China, high energy costs, and lower investment and manufacturing, coupled with a boost in defense expenditure, will continue to suppress growth of the economy and improvement in living standards in Europe.

***

Source for gas costs: Energy News Beat.

Leave a comment