Japan may be running the world’s largest real-time experiment in cognitive finance.

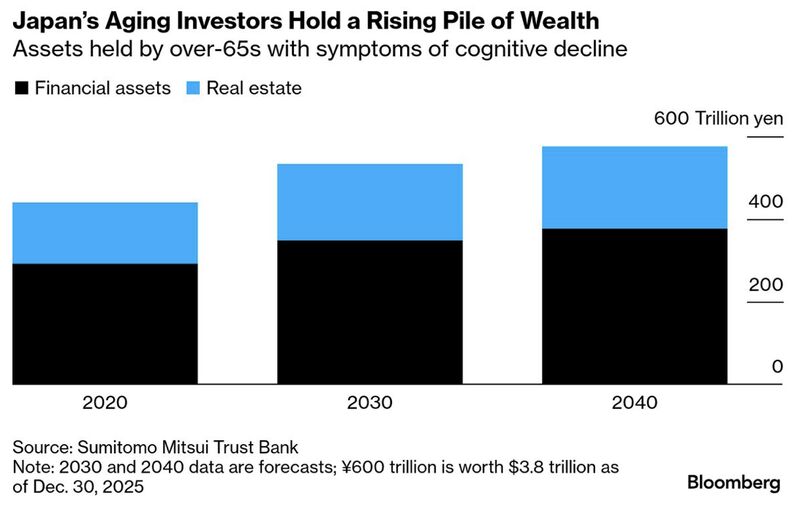

The nation already has about ¥315 trillion (≈$2 trillion) in liquid assets controlled by seniors showing signs of cognitive decline, and this amount is expected to rise materially over the next two decades.

Empirical research shows that individuals tend to underestimate or fail to recognize their own cognitive decline. As a result, financial control is rarely transferred at the optimal time. Transfers are more likely to happen too late rather than too early, and delayed transfers are substantially more costly. Survey evidence suggests that delayed loss of control can reduce household wealth by 10–18%, materially larger than the cost of early delegation.

Banks in Japan are introducing family co-managed accounts not as a convenience product, but as a mitigation tool for predictable decision-making failures. The traditional assumption that individuals will voluntarily step aside when it becomes optimal no longer holds in aging societies.

The macro implication is subtle but important: as the share of wealth held by cognitively impaired investors rises, capital may remain liquid but become increasingly misallocated, with lower portfolio efficiency, slower rebalancing, and weaker transmission of monetary policy through household balance sheets.

Leave a comment